Breakouts led the week while sweet spot setups stayed resilient

Backtest patterns, sweet spot performance, and missed-trade analysis for June 22 to June 26.

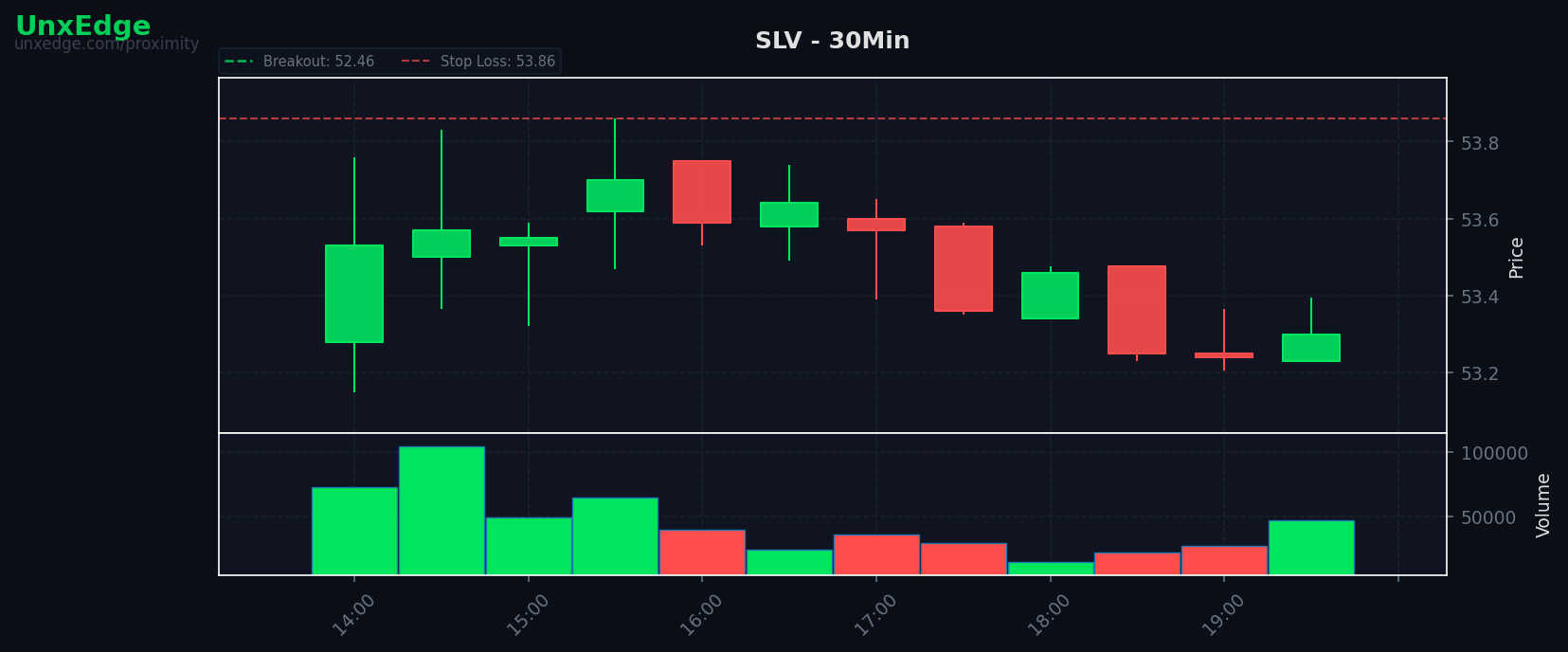

THE EDGE THIS WEEK

Selective strength outperformed broad participation

This week’s data showed a clear split between symbols that trended cleanly once triggered and symbols that repeatedly failed to convert setup quality into follow-through. The broad scanner breakout rate stayed low at 21.4%, while the backtest win rate across active symbols remained much higher at 64.4%, suggesting that signal quality after selection mattered more than raw setup volume.

The dominant pattern was concentration. A small group of names produced highly efficient outcomes, including six symbols with perfect win rates, while several widely followed large caps and sector proxies posted persistent underperformance. In practical terms, the environment rewarded precision and punished generalized breakout chasing.

BY THE NUMBERS

Core market structure metrics

The headline contrast this week was between participation and conversion. The scanner generated 472 setups, but only 101 became breakouts, which indicates that abundance of candidates did not translate into broad directional efficiency. At the same time, the backtest still found a strong aggregate win rate, reinforcing the idea that filtering and symbol selection remained the real edge.

SWEET SPOT REPORT

The 3 to 5 bar low-pressure setup lost its usual advantage

The sweet spot setup, defined as pressure below 60 with a 3 to 5 bar structure, materially underperformed its historical baseline. A 29.7% weekly win rate versus a 58.8% historical win rate is not a small drift. It is a regime-level disconnect between the setup’s normal expectancy and actual realized behavior.

That kind of underperformance usually points to one of two conditions. Either the market offered too little expansion after the trigger, causing otherwise valid bases to stall, or the scanner surfaced low-pressure structures in symbols that lacked true sponsorship. In both cases, the lesson is the same: a favorable pre-breakout compression profile is not enough when follow-through participation is narrow.

For traders reviewing see live setups in the scanner, this week argues for adding a second layer of confirmation beyond the sweet spot definition itself. The setup still matters, but the surrounding context needs to prove that compression is building toward actual expansion rather than just temporary balance.

Research takeaway: when a historically strong setup falls to nearly half its normal win rate, the issue is rarely the setup alone. The issue is usually context selection.

SYMBOL SPOTLIGHT

Where the clearest edges appeared

GDX stood out as the highest-confidence symbol in the dataset. It delivered 16 trades with a 100.0% win rate and a 0.997 average R, which is notable not just for perfection but for sample size. A flawless outcome over that many trades suggests repeatable structure rather than random clustering, making it one of the strongest examples of a symbol entering a sustained alignment phase.

ZM is interesting for a different reason. Its 93.33% win rate across 15 trades and 0.8673 average R show strong consistency without needing perfect outcomes to qualify as elite. This is often the more durable pattern to study. Symbols like this tend to reveal how trend persistence can still create strong expectancy even when not every breakout reaches full extension.

PANW also deserves attention. At 92.86% win rate across 14 trades with 0.8573 average R, it fit the same profile of high-frequency, high-conversion leadership. Taken together, $GDX, $ZM, and $PANW suggest that the best opportunities were not scattered randomly across the tape. They emerged in symbols able to maintain repeated directional acceptance after entry.

On the opposite end, names like COST, JPM, and WMT illustrate what failed. These were not isolated bad trades. They represent repeated inability to hold breakout behavior, which often signals either overhead supply, muted momentum sponsorship, or structurally mean-reverting conditions that make continuation entries inefficient.

WHAT THE BOTS MISSED

Missed opportunity was small in count but large in payoff

The bot miss profile shows an important asymmetry. Only 13 trades were blocked, but they represented +29.3R in unrealized performance, including three runners that reached TP3. That means the cost of missing was not driven by frequency. It was driven by the outsized impact of a few high-quality exclusions.

The fact that every missed trade was blocked by the rvol_threshold filter is especially informative. Relative volume is typically used as a quality control layer, but this week it appears to have been too restrictive in a market where some of the best follow-through occurred without exceptional early volume readings. This does not automatically mean the filter should be loosened across the board. It means the system may need conditional flexibility when other structural variables are unusually strong.

For traders who want to watch the bots in the Edge Lab, this is the main question worth studying next: when does low or moderate relative volume still support an efficient breakout? The answer may sit in combinations such as tighter structure, better sector alignment, or cleaner multiday compression.

Missed-trade analysis suggests the model’s current false-negative problem is more expensive than its raw count implies.

SECTOR HEAT MAP

Breakouts clustered in growth and broad exposure vehicles

Technology led with the highest breakout concentration, posting 24 breakouts, with an additional 6 listed under a duplicated lowercase technology category. Even allowing for category inconsistency, the message is clear: the strongest concentration of successful resolution came from tech-linked names. ETF breakouts ranked second at 11, which often signals that traders were willing to express directional views through baskets rather than relying entirely on single-stock breadth.

Financials, Consumer, and Healthcare each produced 8 breakouts, while Industrials contributed 5. That distribution points to moderate cross-sector participation, but not enough to call the tape broad-based. The leadership profile still appears concentrated rather than evenly distributed.

The duplicated sector labels for Technology and Consumer are also worth noting analytically. When normalized, sector heat would likely show even more concentration than the raw list implies. In research terms, that matters because concentrated breakout success tends to favor traders who rotate into active pockets quickly, rather than those seeking equal opportunity across sectors.

RESEARCH NOTE

Low breakout rate and high backtest win rate can coexist for a reason

One of the most useful lessons from this week is that scanner productivity and trading expectancy are not the same metric. A 21.4% breakout rate looks weak on the surface, yet the broader backtest still produced a 64.4% average win rate across 1,921 trades. The difference implies that edge did not come from taking everything that appeared. It came from rejecting most setups and concentrating in the symbols and structures that repeatedly converted.

This is an important framework for traders. In lower-conversion weeks, the goal is not to force more participation. The goal is to improve discrimination. When setup volume is high but actual breakout efficiency is low, the advantage shifts toward ranking mechanisms, context filters, and symbol-specific behavior patterns. That is why isolated excellence in names like GDX, ZM, and PANW mattered more than the scanner’s raw opportunity count.

The deeper research question going forward is simple: which combinations best identified the small subset of symbols that kept working while the average setup degraded? Answering that will do more for next week’s performance than any attempt to trade more often.