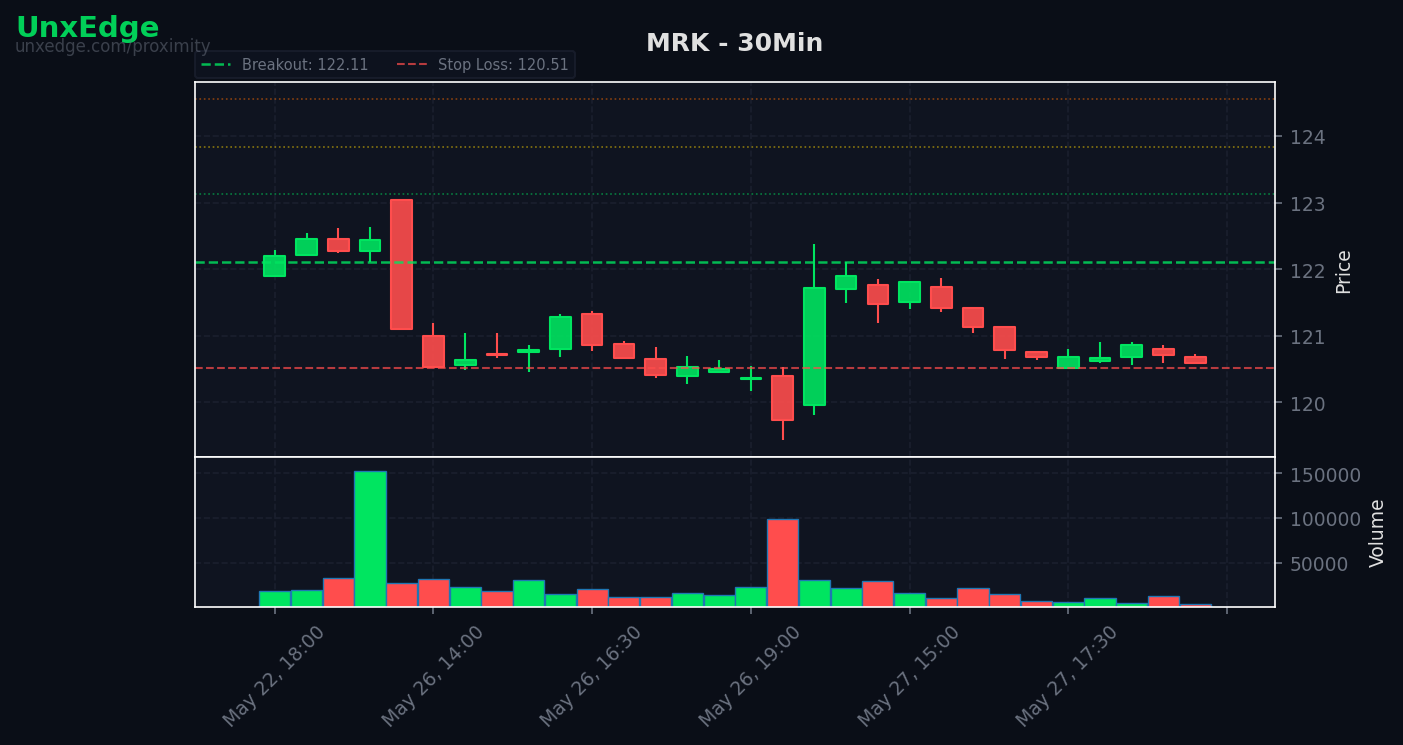

Breakouts drove the week while sweet spot setups stayed selective

Backtest patterns, sweet spot performance, and missed-trade analysis for May 25 to May 29.

THE EDGE THIS WEEK

Selective strength outperformed broad participation

This week’s data points to a market where edge came from concentration, not breadth. Backtests stayed constructive with a 63.1% average win rate across 1,373 trades, but live scanner results showed only a 26.8% breakout rate, suggesting that many apparent setups lacked the follow-through needed to convert into clean momentum trades.

The core pattern was simple: the best results came from symbols that were already capable of sustained trend behavior, while lower quality, lower conviction breakouts failed more often than they resolved. In that environment, trader performance depended less on finding more setups and more on filtering for the right type of setup and the right symbol context.

BY THE NUMBERS

Market structure in the data

The headline divergence this week was between backtested expectancy and live breakout conversion. Historical behavior remained favorable across the tracked universe, but the scanner’s live output was much noisier, implying that entry quality and environmental confirmation mattered more than raw setup count.

That disconnect usually appears when leadership exists, but is narrow. Traders who traded everything likely experienced churn. Traders who focused on proven names and cleaner technical structures likely captured the bulk of the opportunity. For see live setups in the scanner.

SWEET SPOT REPORT

The ideal pressure window underperformed its own history

The sweet spot setup, defined by lower pressure and short 3 to 5 bar structures, posted a 54.8% win rate this week versus a 63.9% historical baseline over 97 trades. That underperformance matters because this is typically the pattern cluster traders rely on when they want balanced participation and manageable risk.

The likely explanation is not that the setup stopped working. It is that the market rewarded cleaner trend continuation in select symbols while punishing average-quality breakouts that looked technically acceptable but lacked enough sponsorship. In other words, the setup logic remained sound, but the week demanded better context selection around it.

When a historically reliable setup underperforms by nearly 9 percentage points, the research question is not whether to abandon it. The better question is what secondary filter would have restored its normal expectancy.

Going forward, the sweet spot should be studied in combination with relative volume and leadership persistence. That matters especially because missed-trade data suggests the system may have blocked some of the very names that would have improved sweet spot performance.

SYMBOL SPOTLIGHT

Where the signal was clearest

GDX stands out because it combined perfect execution quality with sample size. Eleven trades at a 100% win rate and a 0.9985 average R is not just a hot streak. It suggests repeated, orderly continuation behavior where entries were accepted quickly and targets were met without excessive noise. That is the profile of a symbol with stable participation rather than episodic momentum.

PANW showed a similar pattern, also delivering 11 trades with a 100% win rate and a 0.9995 average R. What makes $PANW notable is that cybersecurity strength also showed up elsewhere through FTNT, another 100% club member with 9 trades and a 1.0012 average R. When multiple names from the same thematic pocket produce near-identical outcome quality, that usually points to sector-level sponsorship rather than random symbol-level variance.

SMCI is interesting for a different reason. Its 100% win rate across 9 trades came with a 1.0078 average R, one of the stronger payoff profiles among the top names. That suggests not only a high conversion rate, but also cleaner extension after entry. In practical terms, some names were merely avoiding failure, while others were creating room for larger target realization.

On the weak side, SMH posted 12 trades with just a 33.33% win rate and a -0.3333 average R. That contrast matters. Even while select technology-adjacent names worked exceptionally well, broader semiconductor exposure did not. This reinforces the week’s main pattern: concentrated winners beat generalized sector exposure.

WHAT THE BOTS MISSED

Constraint cost was unusually high

The missed-trade profile is the most important research finding of the week. Only 28 trades were blocked, but they represented +94.5R of unrealized opportunity, including 7 TP3 runners. That is a very large opportunity cost relative to the number of trades excluded.

The dominant blocker was rvol_threshold with 13 misses, followed by spy_alignment with 7, day_pct_filter with 5, and not_on_watchlist with 3. This tells us the system was conservative in exactly the areas where leadership was likely becoming more selective and less index-dependent. In a narrow tape, some of the best names often break before the broader market fully confirms them.

This does not mean the filters are wrong. It means their calibration may be too strict for environments where leadership is concentrated. If the best names are moving independently, then an index alignment requirement can become less protective and more suppressive. Likewise, rigid relative volume thresholds may miss steady institutional accumulation that does not register as explosive participation on the day of the break.

The key issue was not overtrading. It was under-admitting high quality exceptions.

For traders evaluating systematic execution, this is a strong case for adaptive filters rather than static ones. To inspect active automation behavior, watch the bots in the Edge Lab.

SECTOR HEAT MAP

Breakouts clustered in technology and ETFs, but concentration mattered

Breakout counts were led by Technology with 23 and ETF with 20. Consumer categories combined for 23 when standardizing the duplicate labels of consumer and Consumer, while Financials and Industrials each printed 7 and Healthcare posted 6. Even with some category-label inconsistency, the broad message is clear: leadership was concentrated in growth-sensitive and highly liquid instruments.

However, sector totals alone overstate the breadth of opportunity. The symbol-level data shows that not all exposure within a strong sector worked equally well. Cybersecurity names such as PANW and FTNT delivered near-perfect behavior, while broader proxies like SMH struggled. That means the right sub-theme mattered more than simply picking the right top-level sector.

The ETF count is also notable. Elevated ETF breakout activity often appears when traders seek liquid expression of themes but are unwilling to take broad stock-specific risk across the entire universe. That can produce tradable motion, but it can also dilute edge if the underlying stock leadership is uneven.

RESEARCH NOTE

When filters protect less than they exclude

The deeper lesson from this week is that a system can be directionally correct and still leave most of the edge uncaptured. Backtests showed favorable expectancy, elite symbols showed repeatable strength, and missed-trade logs revealed substantial blocked upside. The weak link was not setup generation. It was the boundary between acceptable and exceptional setups.

That boundary deserves focused testing. Specifically, traders should study whether rvol_threshold and spy_alignment should become conditional filters rather than universal ones. If a symbol has a strong historical profile, a clean short base, and sector-level confirmation, then requiring full index alignment or elevated same-day relative volume may reduce capture more than it reduces risk.

In practical terms, the next research iteration should ask one question: which filter relaxations improve participation in high quality outliers without opening the door to lower quality noise? The answer is likely where the next layer of edge will come from.