Breakouts set the pace while the sweet spot stayed selective

Backtest patterns, sweet spot performance, and missed-trade analysis for June 01 to June 05.

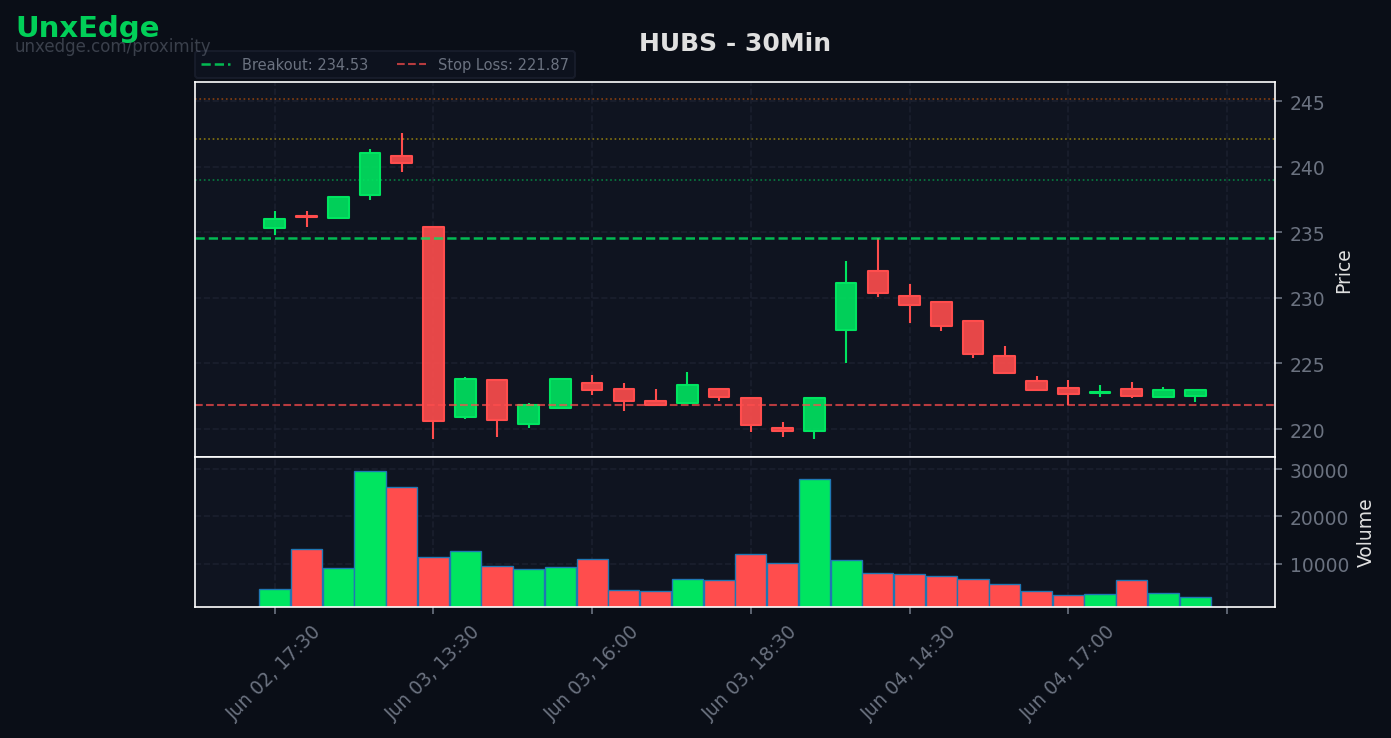

Weekly Research Report: June 01 to June 05, 2026

THE EDGE THIS WEEK

The dominant pattern this week was selectivity. Broad scanner output was active with 408 setups, but only 26.0% became breakouts, which signals a tape where opportunity existed in pockets rather than across the board.

The backtest still held up well at a 63.5% average win rate across 1,500 trades, which suggests the core edge remained intact when applied to the right symbols. The gap between strong backtest performance and weak live breakout conversion points to a market that rewarded precise symbol selection, while punishing broad participation and lower quality continuation attempts.

BY THE NUMBERS

The headline tension this week was simple: internal model quality looked solid, but live conversion rates were less forgiving. That usually happens when the tape supports isolated leaders but does not offer reliable follow through across the average setup. Traders who stayed concentrated in stronger names likely outperformed those treating scanner volume as a broad risk-on signal.

High backtest win rates plus low scanner breakout conversion often indicate a narrowing market. In those conditions, edge comes from ranking setups, not just finding them. To focus on names closest to trigger quality, see live setups in the scanner.

SWEET SPOT REPORT

The sweet spot condition underperformed meaningfully this week. A 44.7% win rate versus a 62.7% historical baseline is not random noise. It suggests that the usual advantage of moderate pressure and shorter consolidation duration did not translate cleanly into expansion.

That matters because sweet spot logic is built around efficient energy release. When that profile weakens, the problem is often not entry timing but post-entry environment. In practical terms, setups may have looked structurally sound but lacked enough broad participation to sustain continuation.

This is a useful reminder that setup quality is conditional. A strong historical profile can still degrade when the market shifts from trend-friendly to rotation-heavy. The research implication is that pressure and bar count alone were not sufficient this week. Traders likely needed an additional confirmation layer such as relative strength persistence, sector participation, or tighter market alignment.

When the sweet spot falls far below baseline, it usually signals a distribution issue, not necessarily a pattern failure. The setup still appears, but the market is less willing to pay it forward.

SYMBOL SPOTLIGHT

Leaders were concentrated, not broad

GDX stood out because it combined perfect backtest execution at 100.0% win rate across 11 trades with repeated scanner presence, showing up four times during the week. That kind of overlap between historical performance and current activity is important. It often marks a symbol where structural behavior is stable enough to keep rewarding the same playbook.

PANW also posted a 100.0% win rate across 11 trades with a near-perfect 0.9995 average R. The takeaway is not just that it won, but that it won consistently without outsized distortion. This is the profile of a clean trend vehicle where execution quality matters more than trying to force larger-than-expected extensions.

INTC deserves mention for a different reason. Its 91.67% win rate across 12 trades was not flawless, but the sample was larger than most of the 100% names. That makes it especially useful from a research standpoint because it suggests repeatability over a broader trade set, which is often more informative than perfection in a smaller sample.

On the weak side, names like UPST, WMT, and IWM reinforce another weekly pattern: lower quality continuation in symbols that either lacked clean directional control or likely faced conflicting flows. The failure cluster was not random. It was concentrated in names where breakouts did not attract enough follow through.

WHAT THE BOTS MISSED

The missed trade profile is one of the most important findings of the week. Twenty-eight missed trades produced +68.9R in unrealized opportunity, including seven TP3 runners. That is a large payoff concentration, which suggests the filters were not just blocking noise. They also blocked a meaningful share of the right tail.

The primary blocker was rvol_threshold with 15 misses, followed by spy_alignment at 12. This tells us the models were conservative in exactly the two places where a narrower market can create friction. Relative volume filters can exclude early movers before participation becomes obvious, and index alignment filters can suppress trades in symbols outperforming a mixed or unsupportive benchmark.

This does not automatically mean the filters should be loosened. It means they should be studied conditionally. In a broad tape, these constraints can protect capital. In a selective tape, they may reduce exposure to the few names actually carrying momentum. The research question is whether dynamic thresholds should replace static ones when leadership narrows.

For traders, the lesson is clear: review blocked setups, especially those rejected on relative volume or index alignment alone. That is where hidden opportunity may have concentrated this week. To compare discretionary logic with automation, watch the bots in the Edge Lab.

SECTOR HEAT MAP

Breakouts clustered most heavily in Technology with 21, followed by ETF structures at 18 plus another 5 logged under a duplicate lowercase category, and then consumer-related groups with 12 and 10 respectively. Financials and Chinese ADRs each contributed 7, while Healthcare posted 6.

The pattern here is concentration in tradable themes rather than uniform sector expansion. Technology leading the breakout count fits the broader idea that leadership was selective and symbol-specific. ETF strength also matters because it often appears when traders prefer expression through baskets instead of single-name commitment, which can reflect either macro uncertainty or theme-driven participation.

The duplicated sector labels in consumer and ETF are a useful operational note. Even with imperfect classification, the directional message is still visible: breakouts leaned toward growth-sensitive and thematic areas, while defensive breadth was less obvious. That kind of clustering supports a narrower opportunity set where sector context improves setup quality.

When breakouts cluster in a few sectors, traders usually benefit from depth over breadth. Instead of scanning everything equally, prioritize the groups already proving they can hold expansion.

RESEARCH NOTE

The key variable was not setup count. It was follow through density.

This week offers a useful distinction between signal frequency and signal quality. There were 408 scanner setups, which is enough to create the impression of abundant opportunity. But only 106 breakouts emerged, and sweet spot performance fell well below historical norms. In other words, the market generated many potential entries without producing enough sustained expansion behind them.

That dynamic changes how traders should think about edge. In a high follow through environment, broad scanning and standard filters are often enough. In a low follow through environment, edge shifts toward ranking symbols by persistence, not just by trigger proximity. The names that worked tended to work repeatedly, while weaker names did not merely underperform. They actively destroyed expectancy.

The practical takeaway is to spend more effort on leadership validation than on setup accumulation. If the market is only willing to reward a narrow slice of symbols, then the research priority becomes identifying which names are repeatedly converting rather than assuming a valid pattern will generalize across the list.